Fixed vs. Reducing Interest Rate: Which is Better for Your Loan?

A comprehensive comparison between fixed (flat) and reducing interest rates. Learn which one saves you more money over time.

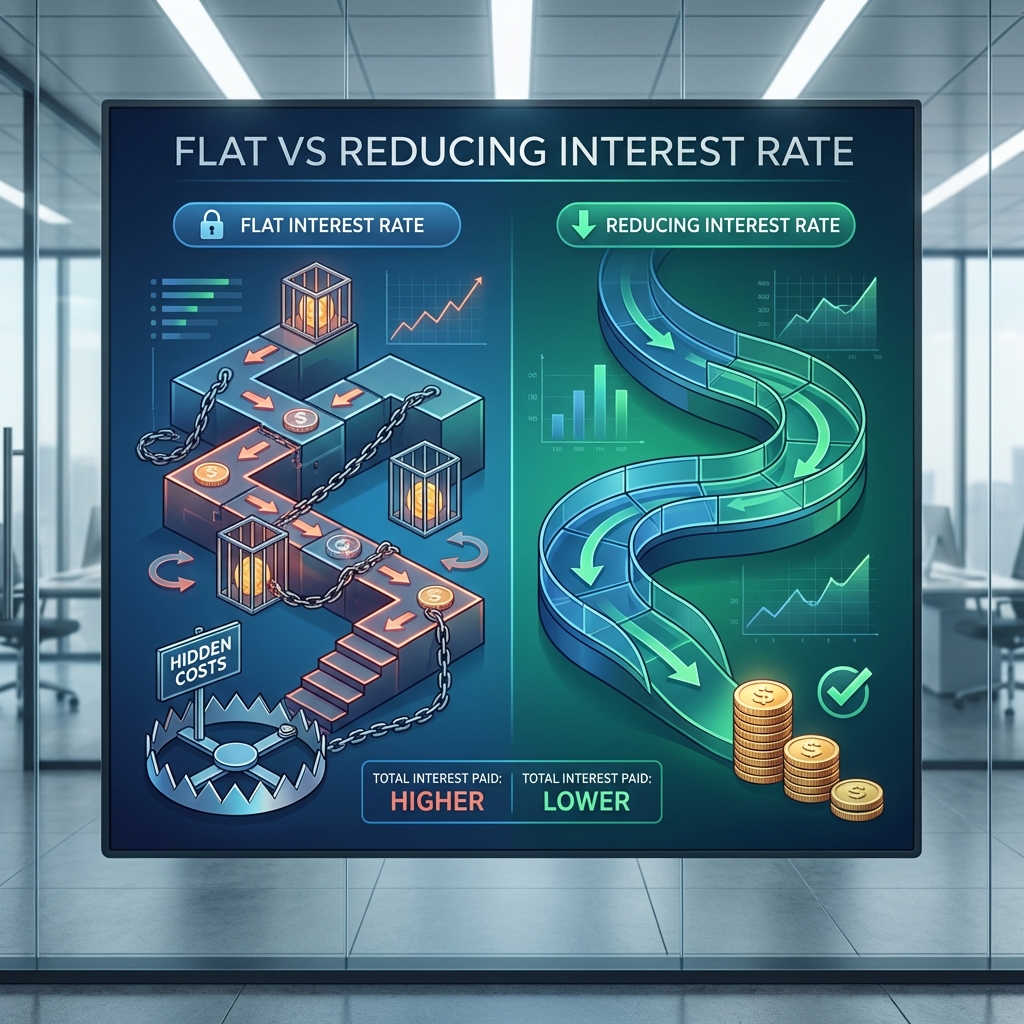

When applying for a loan, the interest rate is often the first thing people look at. However, the way that interest is calculated can be even more important than the rate itself.

What is a Fixed (Flat) Interest Rate?

A fixed or flat interest rate is calculated on the full original loan amount throughout the entire tenure. This means that even as you pay down the principal, you're still paying interest on the money you've already returned to the lender.

Total Interest = Principal x Rate x Tenure

What is a Reducing Balance Interest Rate?

A reducing balance rate is calculated only on the outstanding principal. As you make your monthly payments, the portion of the loan you still owe decreases, and so does the interest charge for the next month.

The Real-World Difference (Example)

Imagine a loan of $10,000 at 10% interest for 3 years:

Flat Rate (10%)

Total Interest: $3,000

Monthly Payment: $361.11

Reducing Rate (10%)

Total Interest: $1,616.19

Monthly Payment: $322.67

The reducing rate saves you almost $1,400 in interest!

Which One Should You Choose?

In almost every scenario, a reducing balance rate is superior and cheaper. Flat rates are often used as a marketing tactic because they appear lower than they actually are. A 7% flat rate might actually be more expensive than an 11% reducing rate.